Home Owner’s Insurance Buyers Guide

Wondering About Homeowners Insurance?

“The most important advice I could give to first-time shoppers is that although home insurance seems pretty simple, it is really anything but,” says Scott W. Johnson, an independent agent with Marindependent Insurance Services.

Maybe you plan to compare homeowners insurance companies on your own. Maybe you’d prefer a more hands-off approach working with an independent agent. Either way, it’s incredibly important to understand the parameters of your policy, and exactly how coverage and payments would shakedown in the event of a disaster.

“As with any purchase, do your own research before you start shopping. Educate yourself so you have a level of comfort with the questions you ask.”Chris Johnston, Personal Injury Attorney at Des Moines Injury Law

This guide covers all the need-to-know information that you should arm yourself with before shopping for a home insurance policy. Are you a brand new homeowner? Don’t sweat it — we’ve covered the most frequently asked questions about homeowners insurance just below. If this isn’t your first time around the block, feel free to skip down the page for advice on:

- Choosing your homeowners insurance coverage

- Choosing your homeowners insurance company

- Other important things to consider

- Homeowners insurance company ratings

- The best homeowners insurance by state

Homeowners Insurance FAQ

What is homeowners insurance?

When a home is damaged by accident or natural disaster, it’s often incredibly expensive to repair or replace. Homeowners insurance protects you from paying those costs out of pocket. In exchange for your annual payment — called a “premium” — the insurer agrees to pay out a much larger sum if your home is damaged by a covered cause. Homeowners insurance costs vary by home, homeowner, location, and company, with states’ average premiums ranging from around $600 to $2,000 per year.

What does homeowners insurance cover?

Homeowners insurance includes coverage for six main categories: Your dwelling (meaning the main house and anything directly attached to it); other structures like garages, fences or guest houses; personal property like furniture and appliances; liability costs and medical bills if someone is injured on your property; and loss of use coverage that can help cover living expenses while your home is being repaired.

How does homeowners insurance work?

Homeowners insurance only pays out on damages caused by something specifically covered under your policy. Within each of the six categories listed above are certain coverages and exclusions; for example, “water damage” is generally covered under dwelling insurance if it’s caused by a burst pipe, but not if it’s caused by flooding. There are 16 common causes or “named perils” that may be covered under homeowners insurance. Which of those 16 perils are covered varies by policy type. Perils commonly covered by homeowners insurance

What does homeowners insurance not cover?

The two big areas not covered by homeowners insurance are flooding and earth movement (which includes earthquakes, landslides, mudflows, and so on). A few private companies sell insurance for these perils, but most homeowners end up getting coverage through federal insurance programs. Other perils not covered by standard home insurance include things like damage from regular wear and tear, fungi or mold, pests, sewer backup, power failure, and “ordinance or law” requiring renovations to meet new codes. Please note that this list is not exhaustive. Exclusions vary by company and by policy type.

Homeowners Insurance Coverage

Know your home’s replacement cost

There are two ways to calculate homeowners insurance limits. Your home can either be insured for its actual cash value (ACV), meaning the market value with depreciation subtracted or replacement cost, meaning the amount that it would actually cost to rebuild your home if it were leveled by a catastrophe.

Insure your home for its replacement cost. That way, if a covered disaster strikes, your insurance company will pay for repairs or replacement in full.

Most homes are insured under an HO-3 policy, which automatically uses replacement cost as the overall coverage amount (also known as your dwelling insurance limit). Keep in mind, though, that you can always opt for higher limits. Coverages for personal property, liability, and other structures are calculated as a percentage of your dwelling insurance — so the higher that limit is, the better coverage you’ll have in all subsequent areas.

Take stock of risks

When choosing coverage, it’s also crucial to think about the types of risks your home will be subject to. Follow the old real estate adage of “location, location, location.” Where you’re located determines, in large part, the likelihood that you’ll have to file a claim, what the nature of that claim will be, and thus which coverages are most important.

There are a few steps you can take to understand your home’s unique risk factors and make sure you’re protected against them:

- Check the home’s claim history: C.L.U.E. (the Comprehensive Loss Underwriting Exchange) is the main database and reporter for claim records. All homeowners are entitled to one free C.L.U.E. report per year. You must own the property to request a report — meaning prospective homebuyers can’t check it themselves, but they can request a report from the seller. This information will show whether the structure or location of the home has caused any past claims that are likely to recur.

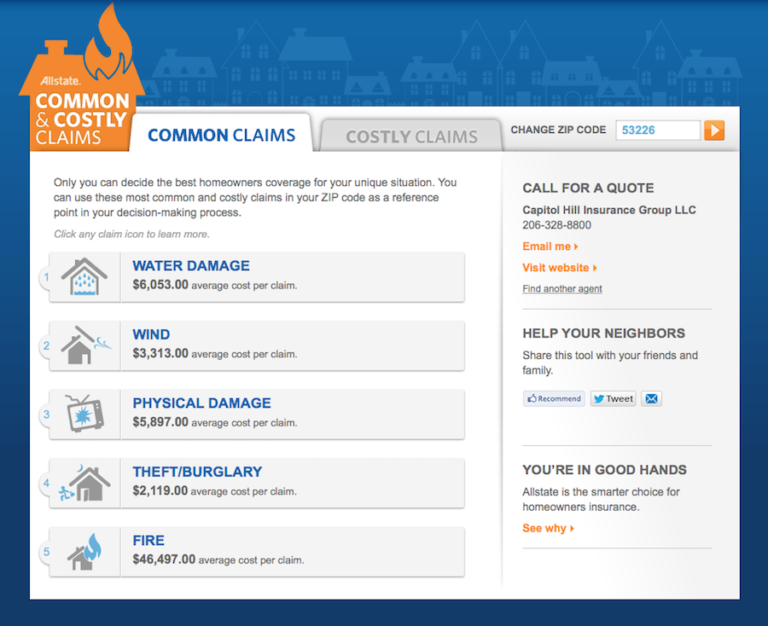

- Check common claims in the area: We recommend using Allstate’s common and costly claims tool, which turns up the most commonly filed claims by ZIP code and how much they cost on average. This will show you which areas of coverage are worth paying special attention to on your policy.

In the 53226 ZIP code of Milwaukee, Wisc., the most commonly filed claim is water damage, but the most expensive claim is fire damage. Source: Allstate.com

To continue reading this Homeowner’s Insurance Buyer’s Guide, click the following Link!

https://www.reviews.com/blog/homeowners-insurance-buyers-guide/

Article by Maggie Overholt, Senior Insurance Editor at Reviews.com

Featured photo courtesy of PD Insurance Agency