Mortgage Rates Skyrocket. New Normal?

The topic of the week has been that rates are going up. They have increased .75% since last week. My preferred lender CNN Mortgage has been crazy busy all week locking in rates for our buyers that she is working with.

I asked Tiffany Taradash to help with an update on the recent rates increases

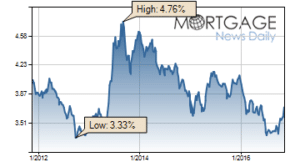

Over the past 3 days, rates have moved higher at a pace that’s only matched by the worst 3 consecutive days of the mid 2013 taper tantrum. There were several days in 1987 where rates moved higher more quickly on an outright basis, but the more recent spikes have constituted much larger proportions of respective ranges. In both cases (1987 and 2013), the recent major highs in rates occurred 6 years early. Simply put, the 2013 rate spike traversed more of its 6-year range than the 1987 spike, and the past 3 days have matched 2013’s pace.

Granted, by the time we look at the weeks and months that preceded the 2 most recent rate spikes, 2013 remains a bigger overall move toward higher rates. But that same caveat is the reason the current rate spike is as scary as it is: we don’t yet know what the coming weeks and months will look like! As recently as last Thursday, quite a few market participants figured that rates had gotten so much higher so quickly, that it surely must have been a knee-jerk reaction to the presidential election that would soon be reversed after the 3-day Veteran’s Day weekend. Yet here we are on Monday with rates still surging higher.

For most of the Summer, rates never moved outside an eighth of percentage point range. Even when rates are trending higher or lower, it typically takes weeks to see a move to the next eighth point increment. Now we’ve seen rates move an eighth of a point higher on EACH of the past 3 business days. This has only happened a handful of times, ever.

Now for the big question: when will this end?

It would be quite useful to be able to accurately predict the timing of these big moves. More often than not, a big rate spike on any given day results in greater-than-average chances of a bounce back toward lower rates–even if only temporarily. Moves like this break the mold though. The price of incorrectly timing the top in rates is steeper than normal as these sorts of moves can often result in rates ‘leveling-off’ as they settle into a new, higher reality. Bottom line: locking still makes sense until and unless we see a substantial move back toward lower rates.

Loan Originator Perspective

Bonds continued their epic selloff today, as rates rose again. In 4 business days we’ve now lost close to 160 bps, a staggering amount, which translates to a rate increase of .75% or more on most loans. Since 2000, I’ve seen this epic scale of “face-melters” twice, in 2004 and the “taper tantrum” of 2013. We’re past the point of hoping to regain last week’s pricing, it’s not going to happen, time to look forward, instead of back. LOCK…..LOCK, and, oh yes, LOCK. –Ted Rood, Senior Originator

Way too much selling, way too fast. Bond markets have priced in a future that includes 2-3 years of a Trump administration successfully transitioning our entire economy. This is way oversold, I am patiently waiting for the markets to come back to reality. It may take some time, but it’s inevitable. I’m floating for now, but closet monitoring the markets. –Gus Floropoulos, VP, The Federal Savings Bank

Ongoing Lock/Float Considerations

- Rates have generally been trending higher since hitting all-time lows in early July, and exploded higher following the presidential election

- Clearly-defined uptrends provide higher-than-average motivation to lock, especially when the pace of rising rates accelerates quickly

- Risk-takers can try to time the dips in rates that may occur during that broader uptrend, but the reward for good timing generally isn’t worth the risk in these situations

- We’d need to see a sustained push back toward lower rates (something that lasts more than 1-3 days) before anything less than a cautious, lock-biased approach makes sense for all but the most risk-tolerant borrowers.

30 Year Fixed Rate Mortgage 15 Year Fixed Rate Mortgage

About This Report

Mortgage News Daily is a trusted source of mortgage rate market data and analysis, with over 1 million readers each month. Unlike many rate surveys, our survey is conducted on a daily basis and is designed to bring you the most current and accurate rate data available. We use a proprietary formula to calculate averages based on best-execution rates from top lender’s rate sheets, also taking into account feedback from hundreds of mortgage market professionals around the country.

Taken from: Mortgage News Daily November 14, 2016