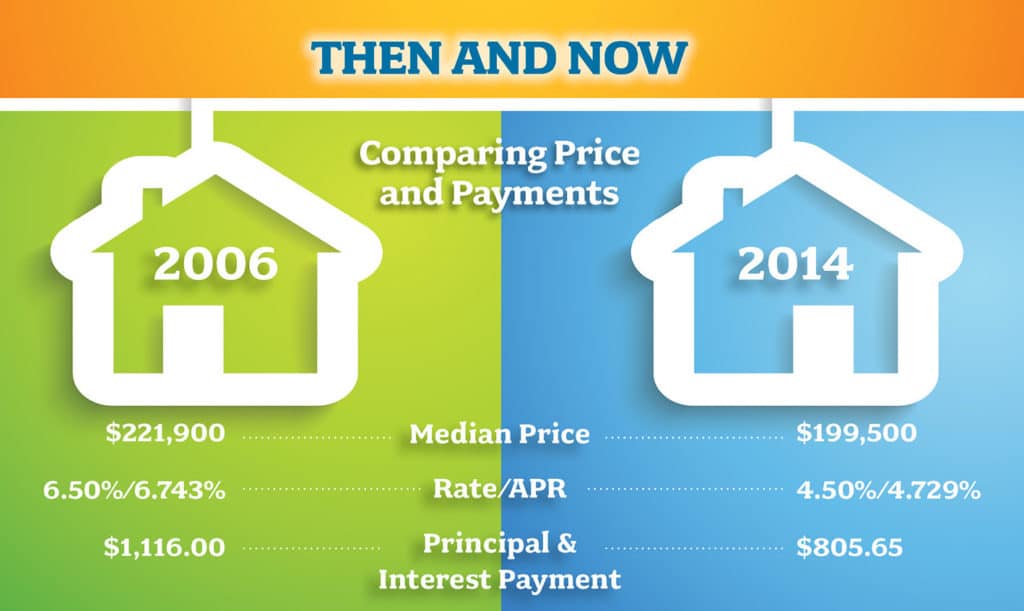

Then and Now – Comparing Prices and Payments

This is an educational example only. Actual current rates are subject to change at any time. Payments shown are for principal and interest on a 30-year, fixed-rate loan. Loan amount assumes a 20% down payment. APR is calculated using closing costs of 3%. Actual fees can be less. Owning a home includes other expenses such as taxes, insurance, maintenance, etc. Qualifying for any loan is based on individual circumstances including but not limited to income, assets, debts and credit history.

Jeremy David Schachter from Pinnacle Capital Mortgage is showing a very simple way to compare then and now.

If you’ve been thinking now may be the time to get into the home market, here are two reasons you may be right:

AFFORDABILITY – The combination of lower prices AND lower rates has the potential to cut mortgage loan payments significantly. You compare the price along with the rate/APR, principal and interest payment for a median priced home.

OPPORTUNITY – The national median price was $176,900 in October 2012 and $199,500 in October 2013. Rates have gone up too. Purchasing at the beginning of these rising trends may prevent further increases in your monthly payment, if you are in the market to buy.

If you are ready to take action – Inventory has fallen from previous levels and in some markets with scare listings, bidding wars have returned. You can act quickly by obtaining pre-approval for your loan. When you do this, sellers will know you are serious and you will have a good idea of the amount you can afford based on payments and costs.

While obtaining a loan may be a more involved process than it was back in 2006, a little bit of knowledge and preparation can help you navigate along the road to home-ownership.

Taken from Jeremy David Schachter, Pinnacle Capital Mortgage.